YOUR BUSINESS AUTHORITY

Springfield, MO

YOUR BUSINESS AUTHORITY

Springfield, MO

Springfield residents are never far away from three things: a car wash, a cashew chicken restaurant and a bank.

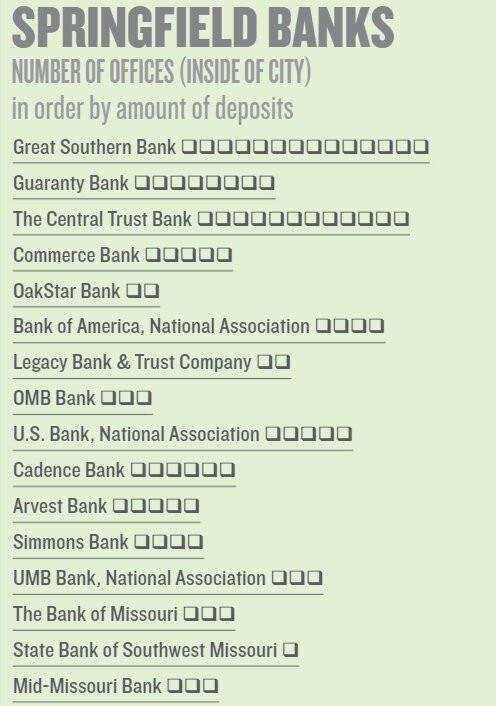

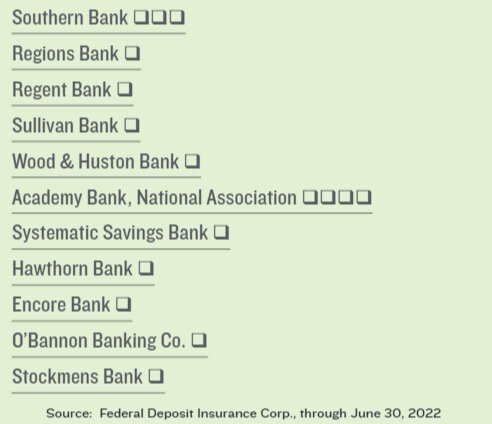

The city has 27 separate banking institutions, each with one to 14 separate offices inside city limits.

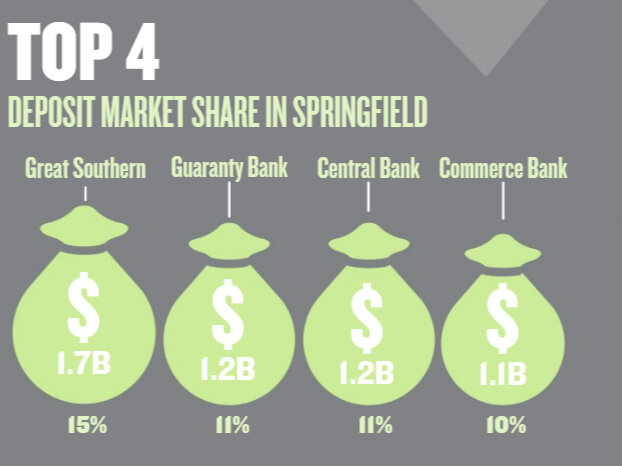

Federal Deposit Insurance Corp. numbers show that as of June 30, 2022, Springfield banks combined had $15.2 billion on deposit with an annual deposit growth rate of 10.4%.

These figures don’t include the nine federally insured credit unions in the city with $1.3 billion on deposit for the same period.

That may seem like a lot of banks. When asked if there were, perhaps, too many, Joe Turner, president and CEO of Great Southern Bancorp Inc., gave a chuckle.

“If you talk to the bankers, they probably all unanimously say yes,” he said.

But Springfield is a stable banking market, Turner said.

“When you look at the numbers – our number of banks, number of offices – it’s been fairly consistent over the last decade or so,” he added.

When considering the number of residents of the city against the number of branch offices, Turner said Springfield is comparable to other larger metro areas in the state.

“I look at the banks in Springfield and think, by and large, they’re all doing well,” he said. “They all seem to be in a good place.”

Back to the question: Are there too many banks?

“I wouldn’t necessarily say Springfield is overbanked, although it is competitive, and that’s generally a good thing,” Turner said. “It keeps bankers on their toes and keeps us focused on improving our business. That’s a very good thing for the customers.”

The more, the merrier

Phelps County Bank is the newest player on the local landscape – so new that it isn’t yet part of the tally of Springfield offices.

The bank plans to open a temporary office this summer as it works to renovate the historic downtown YMCA building at 417 S. Jefferson Ave. for a 2025 move-in, according to past Springfield Business Journal reporting.

In an SBJ report on the Rolla-based bank’s purchase of the Y building, CEO Dominic DeLuca was asked if he saw an untapped market in Springfield, and his answer was no.

“We have competitive instincts,” he said.

He added the move to Springfield was in large part about growing the employee stock ownership plan for the bank, which is 100% employee owned – a category in the nation small enough to be counted on one hand.

With locations in Rolla and St. James, Phelps County Bank had $458 million in deposits, according to June 2022 FDIC figures.

A bank becoming the sole tenant in a four-story historic building may be unusual, but the phenomenon of banks popping up around town is nothing new, acknowledged Brett Magers, president of Legacy Bank & Trust Co. His institution opened a showy new 40,000-square-foot headquarters in 2021 on East Sunshine Street near the intersection with Highway 65.

“It’s always disappointing when people hear another bank is going up on that corner – ‘Another bank! Not a new restaurant!’” he said. “That’s a common theme in the Ozarks. We’re heavily banked.”

Like Turner, Magers thinks the banking landscape is a competitive one. However, he acknowledged that by some measures, there may be too many banks in the city.

“Compared to other small metros, it’s definitely overbanked, if you look at strictly branches per capita,” he said. “That’s true by all matrices the Federal Reserve uses.”

An April report in Financial Times said it was once true that the U.S. had too many banks, particularly regional institutions. The St. Louis Fed counted 14,500 banks in the U.S. in 1984, compared with 355 banks in the United Kingdom.

Since that time, about 10,000 U.S. banking institutions have closed or been taken over, according to the Financial Times, while the nation’s population has grown by a third.

When Congress removed most restrictions on interstate banking two decades ago, banking institutions closed, but the number of branches climbed. That trend has been reversing every year since 2009, according to the FDIC.

By 2021, U.S. banking institutions had declined to about a third of their 1984 tally, with 4,237, or one bank for every 80,000 people. By contrast, Springfield’s 170,000 residents, by the U.S. Census Bureau’s 2022 estimate, are served by 27 banks – which shakes out to 6,296 customers per bank. With 96 bank offices among them, that’s 1,771 customers per office.

Magers said having competition in banking helps consumers by driving up deposit rates.

“We have some of the higher CD rates in the country,” he said. “That’s good for savers.”

Bankrate reported in April that one-year CD rates in Missouri averaged 2.31%, with 18-month rates at 3.09%. A sampling by Springfield banks shows a number of higher-yield offerings, including a 13-month CD at OMB Bank at 5.13%, a 12-month online CD at Guaranty Bank at 4.45%, an 11-month CD at Great Southern at 4.15% and an 18-month CD at Simmons Bank at 3.75%. For borrowers, Springfield’s consumer lending rates are among the lowest in the country, he added.

“That’s really great for the consumer – though it does make it tough as a bank,” Magers said. “Every time there’s a new entrant, there’s only so much business, and they’re all trying to compete for the same great customer.”

Magers said the city has a stable banking market with a stable employment base, due to universities and health care institutions.

“That’s why banks like to do business here,” he said.

Relationship business

With all the competition and numbers, bankers emphasize that relationships matter in banking.

“To a certain extent, our products are fungible,” Turner said. “There are certain ways you can differentiate yourself with product attributes, but the real way we try to differentiate ourselves is with the quality of our people.

“We’ve got almost 1,200 employees, and I think they’re the greatest group of people around.”

Jason England is president and CEO of Arvest Bank in Springfield, which opened a new branch downtown in March.

He described a modern approach to staffing at the branch, with an ambidextrous staffer, trained in all areas of banking, meeting customers at the door and taking care of any business, from a simple deposit to a car loan.

England agreed that Springfield is a strong market, as evidenced by recent entrances to the market by Phelps County Bank and First Midwest Bank.

“It shows the strength of Springfield that other banks want to be located here,” he said.

“It’s a sign of resounding approval for what we’re doing here.”

Springfield Business Journal’s annual Day in the Life feature is back, this time taking you into the day of a health care leader, school district superintendent and brewery owner.